Trying to stay on top of your money can feel exhausting when bills, food shopping, random extras, and everyday spending all seem to come from the same pot.

One minute you think you are doing fine. The next, your bank balance looks lower than expected and you are trying to work out where it all went.

That is exactly why it helps to track expenses properly.

When you know what is coming in, what is going out, and where your money is slipping through the cracks, it becomes much easier to make better decisions. You do not need to become obsessed with spreadsheets or cut out every small treat. You just need a simple way to see what is happening and stay in control.

If budgeting has felt overwhelming, messy, or hard to stick to, this post will help you simplify it. I am going to walk through how to track your spending, how to organise your budget, and how to stop your money disappearing without you noticing.

Why It Matters To Track Expenses

A lot of people think budgeting means restriction. They picture writing down every penny, saying no to everything fun, and feeling guilty every time they buy a coffee.

That is not how I see it.

For me, budgeting is about awareness. When you track expenses, you stop guessing. You start seeing patterns. You notice what is essential, what is creeping up, and what could be tightened without making life miserable.

It also helps reduce stress. Money feels heavier when everything is vague. Once your numbers are clearer, your next steps become clearer too.

Tracking expenses can help you:

- spot where money is leaking each week

- prepare for regular bills properly

- avoid relying on your overdraft or credit

- feel more organised and less panicked

- make space for saving, even if it starts small

That is why this matters. It is not about perfection. It is about making your money feel less chaotic.

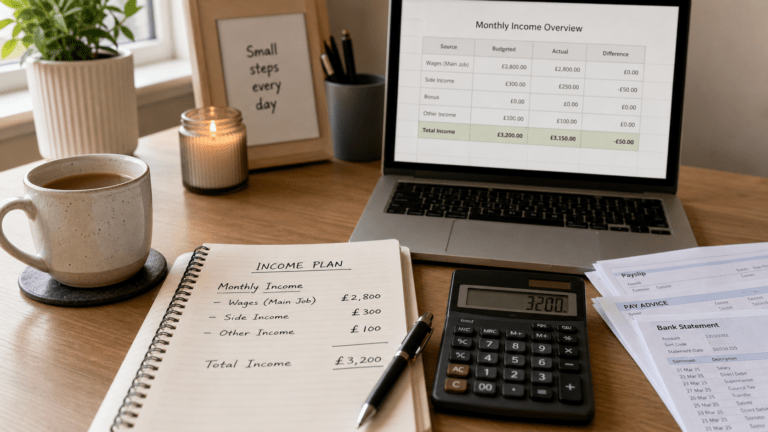

Start With What Is Coming In

Before you look at spending, start with your income.

Write down how much money you have coming in each month after tax. If your income is the same every month, this is easy. If it changes, use your lower average rather than your best month.

This gives you a realistic starting point.

It is tempting to budget from an optimistic number, especially if you sometimes earn extra. But a budget works best when it is built around what you can rely on, not what might happen.

Once you know your true income, everything else becomes easier to plan.

Break Your Spending Into Clear Categories

The next step is to split your outgoings into categories.

This is where a lot of people either overcomplicate things or keep them so vague that the budget is not useful. You do not need twenty tiny categories, but you do need enough detail to see where your money is going.

A simple way to do it is to divide spending into:

Fixed costs

These are the bills and payments that stay roughly the same each month, such as:

- rent or mortgage

- council tax

- gas and electric

- water

- phone

- broadband

- insurance

- loan payments

- childcare

- subscriptions

Variable costs

These are the areas that can change from week to week, such as:

- groceries

- petrol or transport

- takeaways

- toiletries

- clothes

- entertainment

- gifts

- household bits

- personal spending

Financial goals

This category is for the money you want to move forward, including:

- savings

- emergency fund

- debt overpayments

- sinking funds for birthdays, Christmas, travel, or annual bills

Once everything has a place, it becomes much easier to track expenses without feeling overwhelmed.

Look At What You Actually Spend

This part can be eye-opening.

Go through your bank account, card statements, and any cash spending from the last month. Work out what you really spent, not what you think you spent.

This matters because memory is not always reliable with money. Small purchases are easy to forget, especially when they happen in dribs and drabs.

You might think you only bought lunch out twice, but your statement may tell a different story. You may assume your supermarket spend is reasonable, then realise you also did extra top-up shops that pushed the total much higher.

This is not about judging yourself. It is just about getting honest data so you can make better choices.

If you have never done this before, start with one month. That alone can show you plenty.

Build A Budget That Fits Real Life

A good budget has to work in your real life, not your imaginary best-behaved life.

If you make it too strict, you will probably get fed up and ignore it. If you make it too vague, it will not help.

Try giving each category a realistic amount based on what you have actually spent, then adjust where needed. If one area is too high, look at where you can trim it. If you never budget for fun or treats, add a small amount in. A budget with no breathing room often backfires.

If you are still working out the best budgeting method for you, The 50/20/30 Rule: A Simple Guide to Budgeting is a helpful place to start because it gives you a simple structure for dividing your money.

When a budget feels doable, you are much more likely to stick to it.

Check In Weekly, Not Just Monthly

One of the best ways to stay in control is to stop treating budgeting as a once-a-month task.

A monthly overview matters, but a weekly check-in is what keeps you on track.

Set aside ten minutes each week to look at:

- what has gone out

- what is left in each category

- whether any bills are due soon

- whether you need to rein anything in

- whether you can move a little extra into savings

This habit can make a huge difference. Instead of realising too late that you overspent in week one, you catch it early and adjust.

That is often the difference between feeling in control and feeling constantly behind.

Watch Out For The Small Leaks

Big bills matter, of course, but small leaks often do more damage than people realise.

It is usually not one giant spend that throws everything off. It is the repeated little extras that slide under the radar.

Things like:

- grabbing snacks while out

- extra supermarket top-ups

- subscriptions you barely use

- impulse purchases online

- convenience spending when you are tired

- repeated takeaways because there is no plan

These are the areas where it really pays to track expenses closely.

You do not need to cut every single one. But you do need to notice them. Once you see them clearly, you can decide what stays and what needs tightening.

Make Saving Part Of The Budget, Not An Afterthought

A lot of people wait to see what is left at the end of the month before saving. The trouble is, there often is not much left.

Even if it is a small amount, it helps to include savings as part of the plan from the start.

That could mean:

- £10 a week into a savings pot

- a small emergency fund transfer each payday

- setting aside money for annual costs

- building a buffer for unexpected extras

This does not have to be huge to matter. Regular small amounts still count.

If building a safety net feels daunting, Building an Emergency Fund: How to Create a Safety Net on Any Income is a useful next read.

Plan For The Expenses That Always Sneak Up

Some costs are not monthly, but they are not exactly surprises either.

Birthdays, school trips, Christmas, car servicing, MOTs, prescriptions, and annual renewals all have a habit of arriving and wrecking your budget if you have not planned ahead.

That is why sinking funds can be so helpful.

A sinking fund is just a separate pot for a future expense. Instead of panicking when the cost lands, you have already been setting aside a little for it.

Even small amounts help. £5 here, £10 there, and suddenly a once-a-year cost feels much more manageable.

This is one of the easiest ways to make your budget feel steadier.

Keep Your Budget Simple Enough To Stick To

You do not need an elaborate system for budgeting to work.

Some people love colour-coded spreadsheets. Others prefer a notebook, budgeting app, or printable sheet. The best method is the one you will actually use.

If you want extra support with building better habits around your money, Smart Money Moves is a good place to start because it is designed to help you organise your finances in a practical, real-life way without making it all feel complicated.

The simpler your system, the easier it is to keep going. That matters far more than having the perfect setup.

Reduce Spending Without Feeling Deprived

Trying to cut spending by banning everything usually lasts about five minutes.

A better approach is to be honest about what matters to you and cut the things you value least first. That way your budget feels intentional rather than punishing.

For example, you might decide to:

- meal plan so you buy less food you do not use

- reduce top-up shops

- pause subscriptions for a while

- set a weekly fun money limit

- buy less out of boredom

- use cashback or discounts where they genuinely help

If you already shop online for planned purchases, Quidco Cashback: The Secret to Smarter UK Shopping shows how cashback can help you save on spending you were making anyway. It is not a reason to spend more, but it can be a useful extra when used sensibly.

The goal is not to make life joyless. It is to make your spending more deliberate.

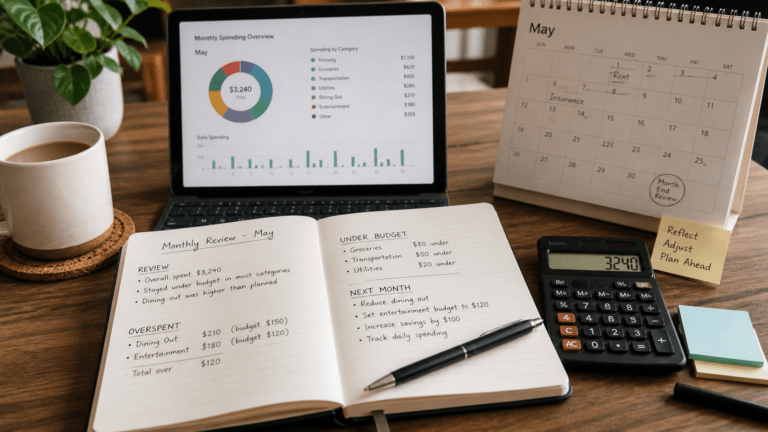

Review And Adjust Every Month

Your budget is not supposed to stay frozen forever.

Prices change. Seasons change. Your priorities change. Some months cost more than others.

That is why it helps to review your budget at the end of each month and ask:

- where did I overspend

- where did I underspend

- what felt too tight

- what felt too loose

- what do I need to change next month

This is where real progress happens.

Budgeting is not about getting everything perfect first time. It is about noticing what is not working and improving it bit by bit.

Common Budgeting Mistakes To Avoid

There are a few mistakes that can make budgeting harder than it needs to be.

Guessing instead of checking

If you do not look at your actual numbers, your budget can end up based on assumptions rather than reality.

Forgetting irregular expenses

Annual bills and seasonal costs still count. If you do not plan for them, they can throw everything off.

Making the budget too strict

If there is no room for real life, it becomes hard to stick to.

Only checking once a month

Weekly check-ins help you catch problems earlier.

Ignoring the emotional side of spending

Stress, boredom, tiredness, and convenience all affect money habits. Budgeting works better when you acknowledge that.

You Do Not Need To Be Perfect To Be Better With Money

This is worth saying clearly.

You do not need to track every penny perfectly. You do not need a flawless budget. You do not need to suddenly become the kind of person who loves admin.

You just need to be more aware than you were before.

If you start to track expenses consistently, even in a simple way, you give yourself a much better chance of staying in control. Small improvements really do add up.

A better budget is built one habit at a time.

Learning to track expenses is one of the most useful things you can do if you want to feel calmer, more organised, and more in control of your money.

It helps you stop guessing. It helps you spot problems earlier. And it helps you build a budget that works in real life, not just on paper.

Start simple. Keep it realistic. Review it regularly. Then adjust as you go.

That is how you build a budget you can actually live with.

What is the easiest way to start tracking expenses?

The easiest way to start is by checking your bank statements from the last month and grouping your spending into simple categories like bills, food, transport, and extras. That gives you a clearer picture of where your money is going.

How often should I track expenses?

Weekly usually works best. A quick weekly check-in helps you spot problems early and make small changes before things get off track.

Do I need a spreadsheet to manage a budget?

No. A spreadsheet can help, but it is not essential. A notebook, budgeting app, or even a simple note on your phone can work as long as you use it consistently.

What if my budget never seems to work?

That usually means the budget is either too strict or not based on your real spending. Start by looking at what you actually spend first, then build a more realistic plan around that.

Can tracking expenses really help me save money?

Yes. Once you can see where your money is going, it becomes easier to spot waste, cut back where needed, and make room for savings.

MoneyHelper budget planner

A useful free tool if you want to break down your income and outgoings in a more structured way. It can help you see what is going where and highlight areas where your budget may need tightening.

Citizens Advice budgeting advice

A good practical resource if you want straightforward help with budgeting, cutting costs, and managing money when things feel tight. It is especially helpful if you need support alongside wider financial pressure.

If this post helped you, share it with someone who needs a money reset or a better budgeting system.

And I would love to know how you keep your budget on track, so leave a comment below and share what works for you.

If you share this post on social media, tag #MissMoneySaver so I can see it.

This post contains affiliate links, which means I may receive a small fee if you sign up for some of the products or services recommended, at no extra cost to yourself.